Projects take place in organizations that are normally applying a form of performance management. Do you know the balanced scorecard, for instance? – “Of course!” You will say. It has been on everyone’s lips for many years and is used in many companies. The performance prism is a related concept that emphasizes the needs of the stakeholders. Although it is not mentioned in PMI’s project management framework, it can be relevant for the integration management and the stakeholder management of a project.

In this article, we provide a short overview of the performance prism concept and discuss its relevance in project management.

What Is Performance Prism?

The performance prism is a scorecard-related and measurement-based performance management concept that focuses on the needs of an organization’s stakeholders.

It was developed by Neely, Adams, and Kennerley at the Cranfield School of Management. The three authors describe their idea in the book “The Performance Prism – The Scorecard for Measuring and Managing Business Success“. The book was first published in 2002. It comprises approximately 400 pages and contains conceptual illustrations as well as numerous practical examples.

The Concept of Performance Prism

There is no question that financial indicators are essential for companies. Also, the customer perspective has established itself as an important area for key figures, for example, through product management, marketing, and customer service.

But can profit, return, equity share, sales, customer satisfaction, and a few more internal key figures alone be the foundation of strategic management?

Neely and his co-authors add a few more dimensions to performance management in organizations. In their view, we must consider all relevant stakeholders for the development of a control system.

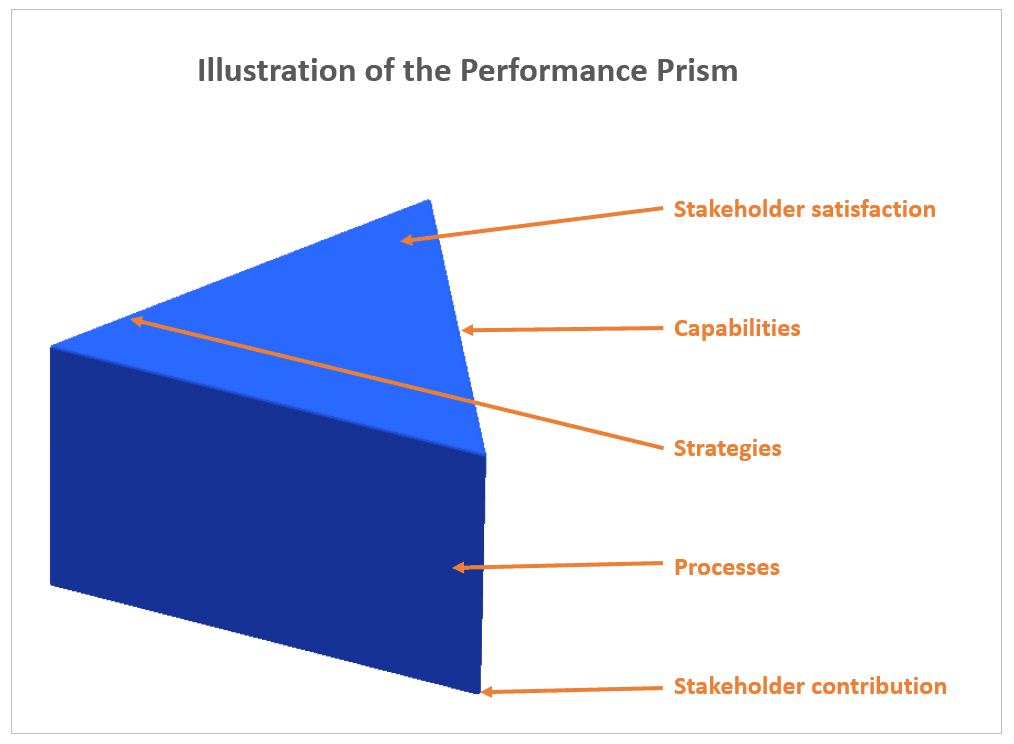

The performance prism consists of five elements (source):

- The satisfaction is the stakeholder form an external view of the business model.

- Internal stakeholders include investors, customers, middlemen, employees, suppliers, legislators, communities, action groups, and partners.

- The internal factors the system considers are strategies, processes, and skills.

- The strategies are based on the stakeholder view and are detailed on the management levels. The processes describe how companies work, with the end-to-end processes spanning several individual methods.

- Measurement dimensions for processes are the quantity, the quality, the time, the user-friendliness as well as monetary values. Finally, the skills of looking at people, technologies are also necessary.

For each stakeholder, the authors carry out a detailed and consistent derivation of critical figures. The result is a success map. The impact chain of measured values is visualized and flows into a central parameter.

Also, a failure scenario is set up using the Failure Mode Test to draw attention to possible adverse developments. It means that both business opportunities and dangers are taken into account.

How Is Performance Prism Used in Practice?

Every company and organization is in an ecosystem of stakeholders that can have more or less influence. Of course, investors want to get a reasonable return on their venture capital, and customers want excellent products and services.

Moreover, investors and customers have other needs and contributions to the success of the company. They also have to take into account other stakeholders, such as employees, suppliers, legislators, communities, and pressure groups.

Therefore, it makes sense to establish suitable vital figures in all of these fields. Establishing a comprehensive and holistic understanding of all stakeholders’ needs is a continuous approach and basis for the organization’s further strategic development. In addition to the strategic goals, the reference points are always the business processes and core capabilities.

You can find a case study of its application here.

Relevance of Performance Prism for Project Management

The performance prism covered is barely covered in common project management frameworks. PMI’s Guide to the Project Management Body of Knowledge (PMBOK) does not mention it at all. However, it can be relevant from two angles:

- For projects that take place in an organization that uses performance prism in strategic and performance management (e.g. in Project Integration Management and as a part of the task of a PMO to align project goals and measures with those of the organization), and

- Applying aspects and learnings from performance prism’s stakeholder focus in a project’s stakeholder management.

Applied in program and project management, this concept strengthens the consideration and implementation of the organization’s overall strategy. Using performance prism can indeed help identify, classify, understand and eventually address the needs of its stakeholders.

It is not only useful for traditional or predictive projects but also in agile frameworks. A number of approaches (e.g. Scrum) suggest that a product owner is the only representative of stakeholders from the business or customer sides in the execution part of a project (e.g. a sprint or iteration). The stakeholders are involved in the presentation of results and increments while it is the product owner’s responsibility to engage and consult stakeholders on an ongoing basis. Adopting ideas and elements of the performance prism concept can therefore facilitate mastering the product owner role.

Conclusion

The performance prism is a stakeholder-focused strategic and performance management system. It can be relevant for projects if they take place in an organization that already uses the performance prism method.

Alternatively, project managers and product owners can refer to some of the aspects of this concept that can be leveraged for their stakeholder communication.

In this context, consider reading our other articles about project communication, balanced scorecard and the role of product owners.